What’s a Rainy Day Fund?

Let’s picture a ‘Rainy Day Fund’ as an umbrella in the world of finance. Just like an umbrella shields you from unexpected rain showers, a Rainy Day Fund protects you from unforeseen financial setbacks.

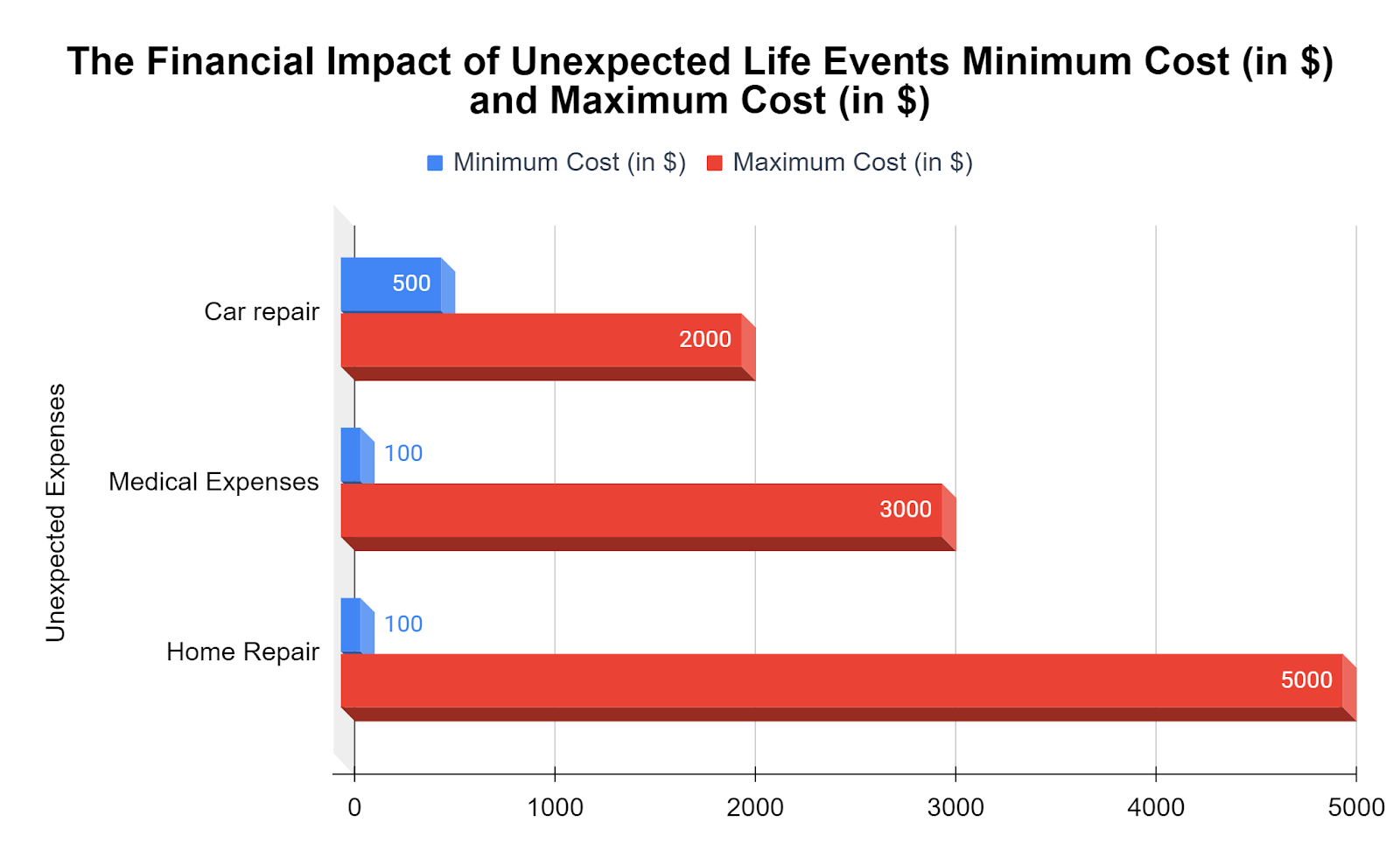

It’s essentially a pot of money you set aside for sudden, unexpected expenses – think car repairs or an urgent medical bill. You hope you’ll never need to use it, but you’ll be grateful for it when you do.

Why You Need a Rainy Day Fund?

Think of it this way – you’re happily sailing along in your financial boat, and then you hit an iceberg named ‘Unexpected Car Repair’. A Rainy Day Fund is like a lifeboat that keeps you afloat.

Imagine if your car, the ‘ol reliable, decides it’s a good day to take a permanent vacation. Or maybe, your refrigerator decides to retire prematurely. To cover these unexpected costs, we build our financial Noah’s Ark, the rainy day fund.

A Rainy Day Fund provides a financial buffer against uncertainties. Without one, you might need to rely on high-interest loans or credit cards, creating debt and stress. Imagine it as a shock absorber in your financial vehicle, making the bumps on the road of life smoother.

How Much Should You Save?

“Always be prepared” is not just a Boy Scout motto; it should be your mantra when it comes to personal finance. A good rainy day fund should be enough to cover your living expenses for three to six months.

To find your magic number, add up your essential monthly expenses, like your cable bill, your mouth-watering pizza delivery tab, or that cute dog walker’s payment (you know, the necessities). Then, multiply by three to six. Voila, there’s your target!

Now, before you pass out at the size of that number, remember the wise words of financial guru Lao Tzu (not really, but stick with us here), “The journey of a thousand miles (or dollars) begins with one single step (or cent).”

So, you might be asking, “How big does my financial umbrella need to be?” Ideally, your Rainy Day Fund should be enough to cover 3-6 months of living expenses.

Easy Steps to Start a Rainy Day Fund

Ready to build your financial shield? Let’s break it down into easy, digestible steps:

Setting Your Sights: How Much to Save?

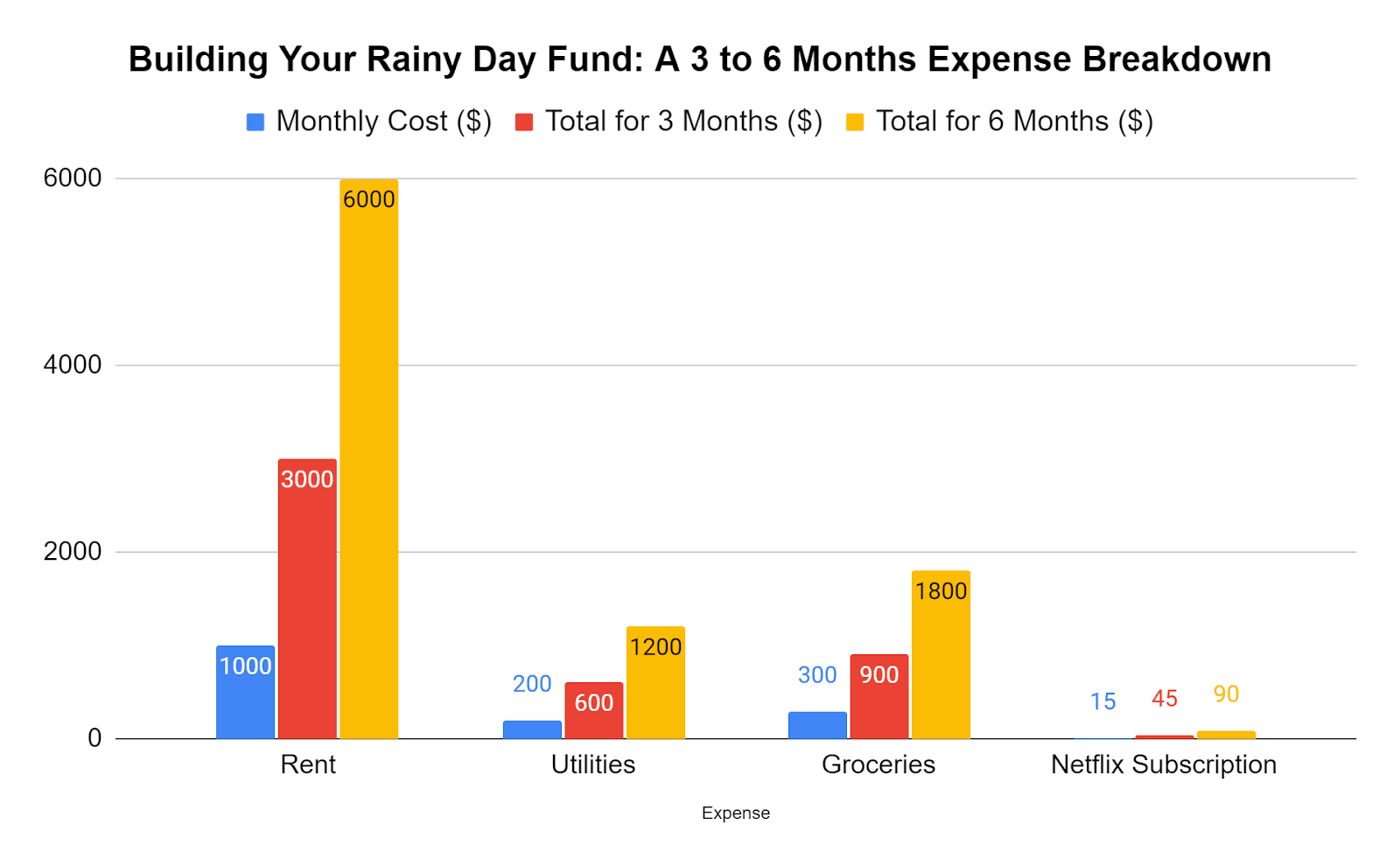

As a rule of thumb, a well-stocked rainy day fund should hold enough to cover 3-6 months of expenses. But remember, this isn’t a sprint; it’s more like a leisurely stroll through the park.

Consider this: if your monthly expenses are around $2000 (rent, utilities, groceries, and let’s not forget your Netflix subscription), then you’re aiming for a sweet spot between $6000 to $12000. Sounds like a pretty penny, doesn’t it? But fear not, brave financial adventurers!

Small Steps Lead to Big Savings

When you’re facing the financial Mount Everest, it’s essential to remember that every journey begins with a single step – or in our case, a single cent. If the saving target seems like the final boss in a video game, remember, every coin you toss into your savings is a victory.

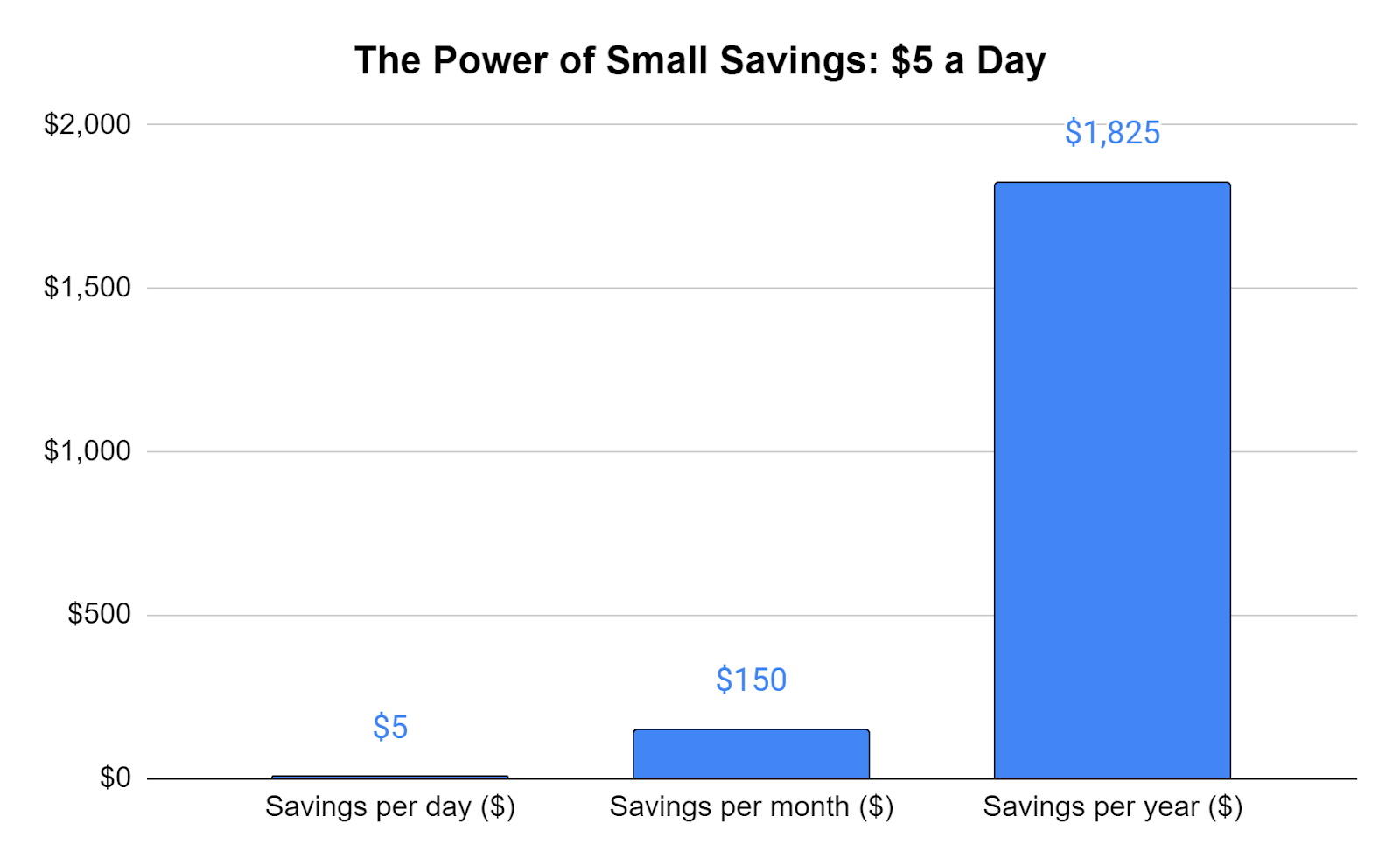

So, let’s say you start by saving just $5 a day. It might not seem like much, right? But like those sneaky calories in your favorite donut, they add up. In a year, you’d have saved $1825, without breaking a sweat.

Or Take the 52-week Challenge

Let’s go on a fun little journey, shall we? Let’s call it the “52-Week Road to Riches”. The idea is simple: It starts as a tiny snowball and ends up as a massive avalanche of savings.

Here’s how it works: First, think of the smallest bill in your wallet. Got it? That’s right, it’s that lonely $1 bill. Now, take that bill and put it into your Rainy Day Fund. Congratulations! You’ve just started your journey to the land of savings. That was the first week.

Now, onto week two. Double up! Take two of those $1 bills and add them to your fund. Things are getting interesting, aren’t they?

As the weeks roll on, you keep adding another dollar. So, $3 in week three, $4 in week four, and so on. Like a snowball rolling down a hill, your savings grow bigger and bigger each week.

By the time you reach week 52, you’re tucking away $52 into your fund, and guess what? You’ve got a pretty little sum of $1378 in your Rainy Day Fund! And all this without having to give up your daily latte or Netflix subscription.

This strategy turns saving into a fun game. It’s like playing Monopoly, but instead of fake paper money, you’re dealing with your real, hard-earned cash. So, put on your top hat, hop into the race car, or grab the wheelbarrow, and let’s get saving!

The Magic of Automatic Transfers

Now, onto our secret weapon – automatic transfers. They’re like your financial fairy godmother, quietly working magic in the background.

By setting up an automatic transfer from your checking account to your savings, you’re building your rainy day fund while you sleep. It’s like having a virtual piggy bank that fattens itself.

Just imagine – what if our friend Bob, instead of spending $100 on a new pair of sneakers, decided to toss that into his savings? After a year, with the magic of compounding, he could have a tidy sum nestling in his account.

Isn’t that cool? Just like those abs we all want, building a solid rainy day fund takes time and consistency. But with these easy steps, you’ll be well on your way to weathering any financial storm.

Keeping Your Rainy Day Fund Secure and Accessible

Choosing the right home for your Rainy Day Fund is crucial. It should be secure and easily accessible. Think of it like choosing a pet’s home – safe, comforting, and easy to reach.

A high-yield savings account or a money market account could be good options. The idea is to keep this fund liquid and easily accessible, so you won’t have to wait for days or sell investments when you need the money most.

Here’s an interesting fact: Did you know that Google’s parent company, Alphabet Inc., holds over $100 billion in cash reserves? Talk about a massive Rainy Day Fund!

Curious to find more about the best ‘financial kennels’ for your Rainy Day Fund? Hold your horses! We’re going to dive deep into this topic in our next blog. Check out the sneak peek of our upcoming post, “Where to Keep Rainy Day Funds?” You won’t want to miss it!

FAQs

Why is it called a rainy day fund?

Great question! The term ‘Rainy Day Fund’ might bring to mind images of clouds, umbrellas, and staying indoors, but its financial meaning is a little different, yet quite straightforward.

1. A Metaphoric Umbrella: Just as you’d use an umbrella to stay dry during an unexpected downpour, a ‘Rainy Day Fund’ is essentially financial protection against unforeseen circumstances. These could be anything from sudden car repairs, medical expenses, or even job loss. It’s a cushion for those stormy, unforeseen life events.

2. Simple Language: In its essence, a ‘Rainy Day Fund’ is a pool of savings that you set aside strictly for emergencies. It’s like a financial safety net. Simple, right?

3. Well-Structured Fund: Your ‘Rainy Day Fund’ should ideally hold enough money to cover three to six months’ worth of living expenses. It’s structured in a way that you can dip into it without derailing your long-term financial goals or having to rely on credit.

4. Current Relevance: With the ups and downs of the economy, having a ‘Rainy Day Fund’ is more important than ever. It provides a sense of financial security, ensuring you can weather any unexpected financial storm.

5. Consistent Tone: Remember, building a ‘Rainy Day Fund’ doesn’t have to be a daunting task. Start small and keep adding to it. Over time, it’ll grow into a sizable safety net.

And just like carrying an umbrella gives you peace of mind on cloudy days, having a ‘Rainy Day Fund’ will help you sleep better at night, knowing you’re prepared for life’s financial storms.

6. User-Focused: Every individual’s financial situation is different, but one thing remains constant: the need for a financial safety net. A ‘Rainy Day Fund’ is one size fits all; whether you’re a recent college graduate or a seasoned professional, everyone can benefit from having one.

Hope this clarifies your query! If you have more questions, feel free to ask. Our aim is to make finance easy and accessible for you.

How should I invest my rainy day fund?

That’s an excellent question! Investing your Rainy Day Fund is all about balance – between safety, accessibility, and growth. Let’s dive into it.

1. Safety First: The primary goal of your Rainy Day Fund is to serve as a safety net during financial emergencies. So, it’s important that these funds are kept in a low-risk account where your principal is safe.

2. Ready When You Are: Emergencies don’t operate on a timetable, they can occur at any moment. Therefore, you should keep your Rainy Day Fund in a liquid form that you can easily access without delay, such as a checking or savings account.

3. Simple Savings: Given its purpose, the best place for your Rainy Day Fund isn’t necessarily in an investment that can fluctuate with market conditions. Instead, consider options like high-yield savings accounts or money market accounts that provide a modest interest rate while keeping your money readily accessible.

4. Smart Structure: The key to a well-structured Rainy Day Fund is to keep it separate from your everyday checking account to avoid the temptation to dip into it. It should also be separate from your long-term investments.

5. Current and Correct: As of now, some high-yield savings accounts offer up to a 1.00% annual percentage yield (APY), making them a good choice for storing your Rainy Day Fund. However, always check the most recent rates and account terms before deciding.

6. Consistent Tone: Investing your Rainy Day Fund may not offer the thrilling returns of the stock market, but remember, the objective here is to preserve capital and ensure easy access. It’s like keeping a spare tire in your car – not exciting, but vital when you need it!

7. Focused on You: Ultimately, the best option for your Rainy Day Fund will depend on your individual financial circumstances, risk tolerance, and comfort level. If you’re unsure, consider consulting with a financial advisor to explore what would work best for you.

I hope this helps clarify things! If you have any other questions, feel free to reach out. We’re here to guide you on your financial journey.

What are some examples of rainy-day funds?

Great question! Rainy Day Funds, also known as emergency funds, come in different forms and sizes based on personal situations. But, they have one common goal – to provide a financial cushion when life throws a curveball. Let’s look at some examples:

1. Individual Rainy Day Fund: Let’s say you’re a software developer, and you’ve squirreled away $10,000 in a high-yield savings account. This fund could cover unexpected expenses like car repairs, a sudden health issue, or tide you over in case of job loss.

2. Family Rainy Day Fund: Suppose you have a family with two kids. You’ve managed to save up $25,000. This fund could come to your rescue if the roof suddenly leaks or there’s an unexpected family health emergency.

3. Small Business Rainy Day Fund: Imagine you own a small coffee shop. You’ve saved up an equivalent of six months of operating expenses. If the coffee machine breaks down or business slows due to unforeseen circumstances, this fund could help keep the doors open

4. Freelancer’s Rainy Day Fund: As a freelancer, your income might fluctuate. So, you’ve accumulated a fund that can cover 3-6 months of expenses. This could help during dry spells when assignments are scarce.

5. Retiree’s Rainy Day Fund: You’ve recently retired and have set aside money that could cover sudden medical expenses or emergency home repairs, without dipping into your retirement savings.

6. The Big League Example: At the corporate level, consider Google’s parent company, Alphabet Inc., which holds over $100 billion in cash reserves. While not technically a ‘rainy day fund’, this reserve ensures they can weather any financial storm.

Remember, the size and form of your Rainy Day Fund will depend on your individual circumstances and needs. It’s your personal safety net. And like any good safety net, its primary job is to be there, strong and ready, when you need it the most.

If you’re keen on learning more about smart budgeting, you may want to explore our previous article titled: “Budgeting Activities for College Students”

In this guide, we have clearly explained the 50-30-20 budget rule – a simple yet effective budgeting strategy that can help you manage your expenses in a balanced way. By following this rule, you can learn how to allocate your income for necessities, wants, and savings. Do give it a read for more insights!