Introduction to Life Insurance

Life insurance, in essence, is a contract between an individual and an insurance company. The person agrees to pay premiums, and in return, the insurance company commits to provide a payout, known as a death benefit, to beneficiaries upon the insured person’s death. It is also crucial to understand the role of life insurance in estate planning.

Think of it like a savings jar. Every month you put a little money in it (your premiums), and when you are not around anymore, your loved ones can open the jar and use what you’ve saved (the death benefit) to meet their financial needs.

The Concept of Estate Planning

Estate planning is like an elaborate, well-crafted letter to your future self and your loved ones. It ensures your assets are distributed according to your wishes after your demise. It can include your home, investments, business, and yes, even your life insurance policy.

Imagine you have a pizza (your estate) that you want to share after you’re gone. Without a proper plan (estate planning), there might be a brawl over who gets what slice. With a plan, you leave clear instructions on who gets which slice and how much.

Interplay of Life Insurance and Estate Planning

Here’s where we unite our two-star players – life insurance and estate planning. Life insurance is running the bases, ensuring financial security for your loved ones when you’re no longer around. Meanwhile, estate planning is your game strategy, detailing how your assets will be allocated after your departure.

Consider life insurance as the secret ingredient in your estate planning soup. It can serve a vital role by adding liquidity to your estate when the heat is on – when you need to settle your debts, pay taxes, or cover other expenses upon your death..

Think of it as a sprinkler system kicking in during a fire. If you owe money or have significant expenses when you depart, your life insurance payout can douse those financial flames without needing to sell off your assets.

Let’s dive into a real-world example. Picture John, your friend who’s been kneading dough and baking bread all his life. He’s got a successful bakery business that has fed him, his family, and his local community. He also has a lovely house with a white picket fence and a fancy car parked in the driveway. Sounds nice, right?

But behind this picturesque scene, John also has significant business loans he took out to grow his bakery.

John’s life insurance comes into play when he hangs up his apron for the last time. After his passing, his life insurance payout provides the much-needed dough to settle his debts. This way, his family won’t have to consider selling off the family bakery, the house, or that fancy car.

In essence, life insurance serves as a financial buffer, a security net, or a fiscal superhero (no cape, though) that can keep your estate intact, helping your loved ones manage their finances better after you’ve bid your final adieu.

It’s wise to weave life insurance into your estate planning tapestry to ensure the best possible financial outcome for your beneficiaries.

Remember when Yahoo was acquired by Verizon in 2017? Upon their demise, the Yahoo shareholders could leave their acquisition profits to their beneficiaries via a life insurance policy without worrying about estate taxes eating into their wealth.

The Importance of Life Insurance in Estate Planning

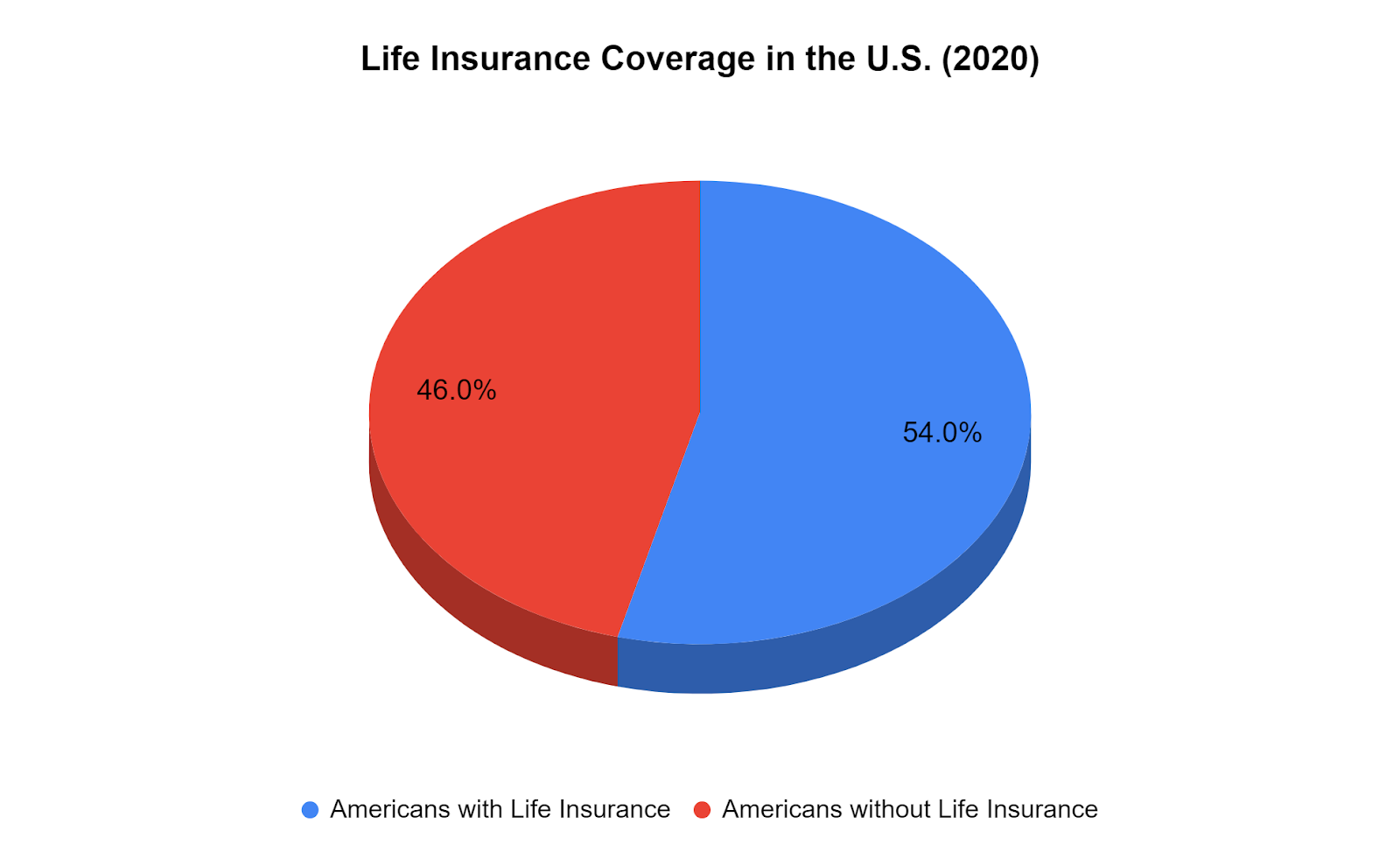

In 2020, according to a study by the Insurance Information Institute, about 54% of Americans had life insurance. Why? Because life insurance brings peace of mind, knowing your loved ones won’t have to scramble or make tough decisions while they’re grieving.

According to Forbes 2023, the majority of Americans, approximately 75%, have some form of life insurance, yet around 80% of us are in the dark about the true costs. It seems that misconceptions are common; for instance, many don’t realize that personal history factors like driving records, credit history, and even past criminal offenses can play a significant role in determining insurance quotes.

Well, life insurance is that comforting cup of hot chocolate on a stormy night. It brings peace of mind, knowing that if life throws a curveball, your loved ones won’t be left scrambling in the financial dirt. They won’t have to make lightning-fast, tough decisions amidst their grieving.

In addition to being a financial cushion, life insurance serves another purpose in the grand scheme of estate planning. It can allow your beneficiaries to sidestep probate – a process that’s as enjoyable as stepping on Lego pieces in the middle of the night.

Probate is a public, often lengthy legal procedure, where your estate is administered. It can be a stressful, time-consuming process and not something your loved ones would want to be tangled in while they’re in mourning.

But here’s where life insurance shines. When life insurance is incorporated into your estate plan, it can offer an express lane for your beneficiaries.

They can bypass the snaking queues of probate, gain immediate access to the life insurance payout, and use these funds to settle any pressing bills or financial obligations.

So, the role of life insurance in estate planning? It’s like a well-placed safety net under a tightrope. Even if life’s balance is upset, this safety net can prevent a financial freefall, providing a secure landing for your loved ones.

It’s not just about peace of mind; it’s about a strategic move for protecting your legacy and your loved ones’ financial future.

Closing Thoughts

No matter how big or small your estate is, life insurance can play a vital role in ensuring your assets are distributed according to your wishes. It can help your beneficiaries bypass probate and give them immediate access to the funds they may need to meet their financial obligations.

The key is to work with an experienced financial advisor who can guide you on the most suitable life insurance policy based on your unique circumstances.