You might wonder, “Is it akin to wrangling my unkempt lawn on a weekend?” Well, not quite, but both endeavors can save you a nice chunk of change! Did you know what is a mortgage and how to negotiate a lower interest rate on your mortgage?

Understanding Your Mortgage: Decoding the Code

Navigating the financial seas of homeownership can be a complex endeavor, but at its heart lies a relatively simple concept: a mortgage. A mortgage is a special type of loan that you obtain to purchase a property. It involves borrowing a large sum of money, the principal, from a lender and then paying it back in increments over an extended period of time, typically 15 to 30 years.

Along the journey, you’ll meet companions like interest, the cost of borrowing the principal, and terms like ‘early principal payments’, which can help you vanquish your debt sooner. Yet, the world of mortgages has many more nuances and depths to explore.

To dive deeper into this realm and understand key concepts like the effects of paying extra on your mortgage principal, check out this comprehensive guide.

Why Negotiate?

Have you ever considered negotiating? Oh, I don’t mean haggling over prices at a flea market. No, my friends, we’re talking about negotiating the interest rates on your loans. Think of it like playing chess with your bank, but instead of checkmating your opponent, you’re looking to shave off a few percentage points.

In simple terms, negotiation is the art of persuasion. It’s about talking your way into a better deal. Just imagine trying to convince your gym instructor to let you skip the last set of crunches, but this time you’re trying to persuade your bank or lender for a better interest rate.

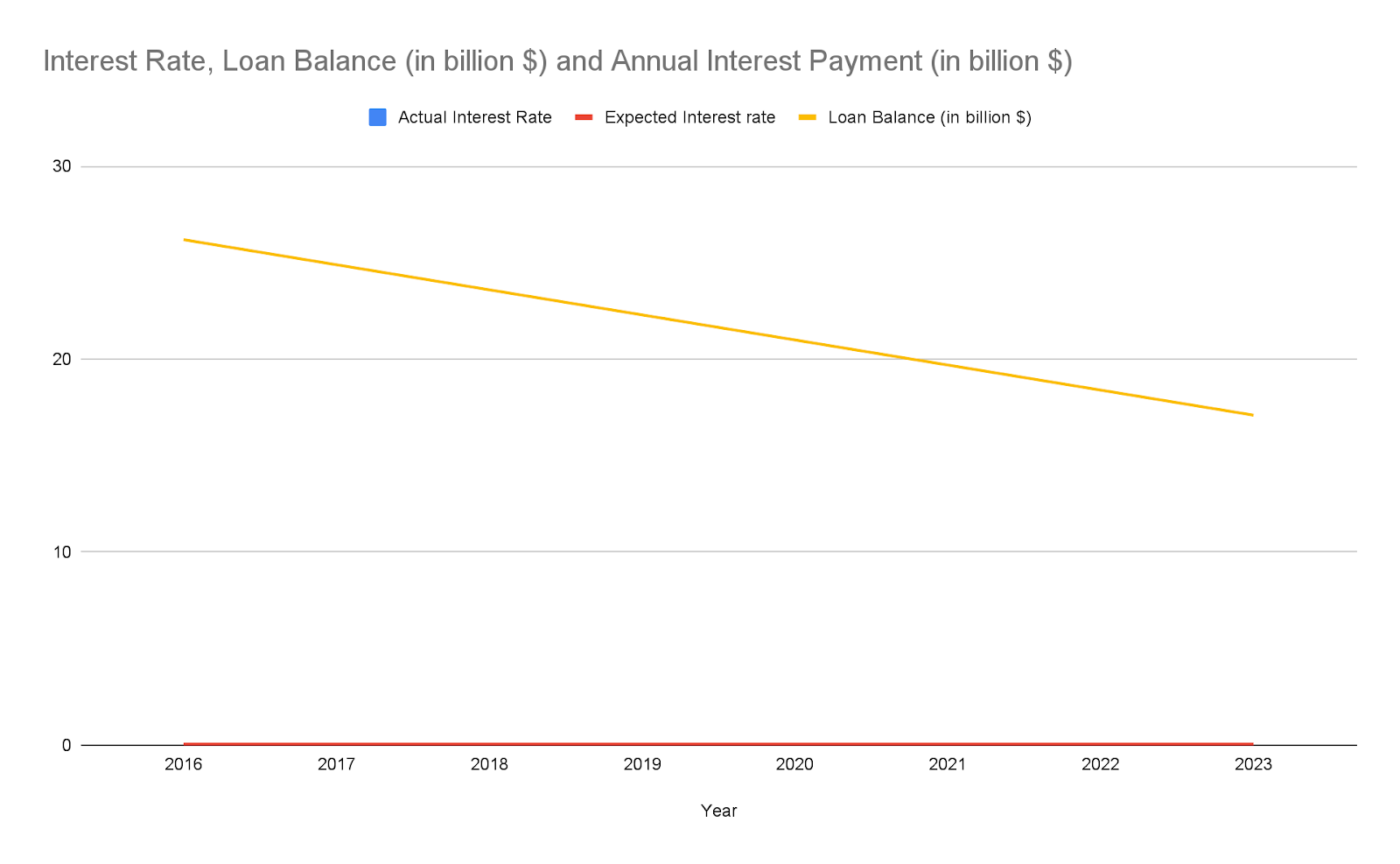

Let’s dive into an example. Remember when tech giant Microsoft acquired LinkedIn back in 2016? What if Microsoft, instead of paying $26.2 billion upfront, decided to negotiate a better interest rate for their loan?

Even a 0.5% reduction could have saved them millions in the long run. It’s a bit like finding a forgotten $100 bill in your pocket but with a few more zeroes!

Don’t be shy about negotiation. It’s not about nickel and diming; it’s about optimizing your financial future. Because the next time you consider taking a loan, remember there’s a potential treasure chest of savings hidden right under your nose. You just have to negotiate to find the key.

Remember, every percentage point counts when it comes to your financial health. So put on your negotiation boots, have a chat with your lender, and start digging for that financial goldmine!

Preparing for the Negotiation

Picture this: you’re a superhero. A money-saving superhero, to be precise. Your mission, should you choose to accept it, is to tackle the notorious villain—Interest Rates.

This isn’t a walk in the park, folks. It’s more like walking a financial tightrope, and you’ve got to balance your act. That’s where your credit score enters the picture. Think of it as your superhero reputation. The higher it soars, the more people trust you; the same applies to banks.

Remember Clark Kent from Smallville? Imagine if he had a stellar credit score. Now, even with his alien origins, if he were to walk into a bank, they’d roll out the red carpet! A higher credit score signals lower risk, which translates to lower interest rates on loans.

But even superheroes don’t walk into battles blindfolded. They do their homework. So, next up, gather intel. That means researching interest rates offered by different banks, financial institutions, and credit unions. It’s like doing a Google Maps search before heading out—you need to know your destination.

Ever seen Iron Man without his suit? Exactly. So suit up! That means understanding your financial health like the back of your hand. Do you remember when Tony Stark in the Marvel universe was dealing with his company’s stocks? He didn’t wing it. He did his research. He knew his financial standing.

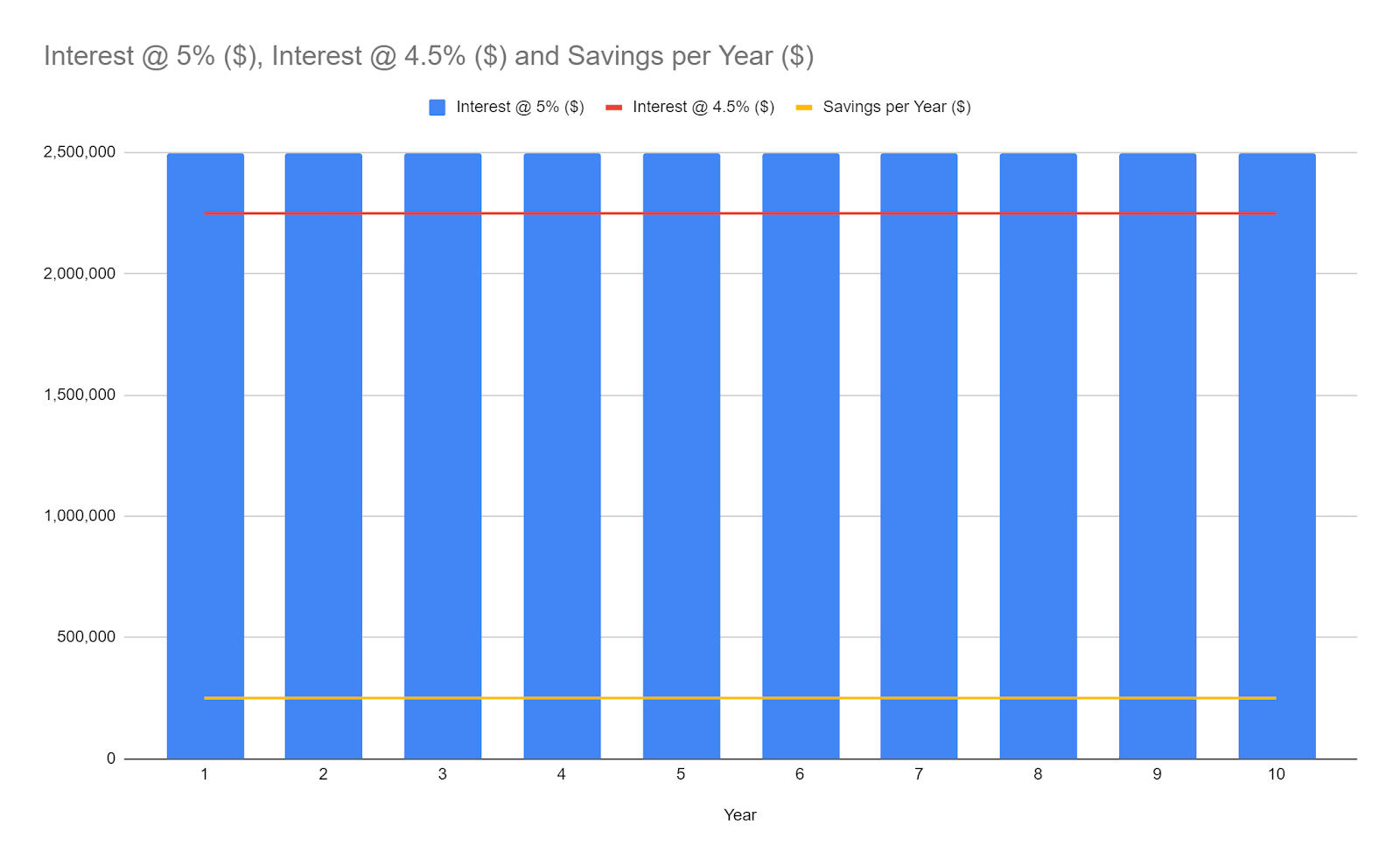

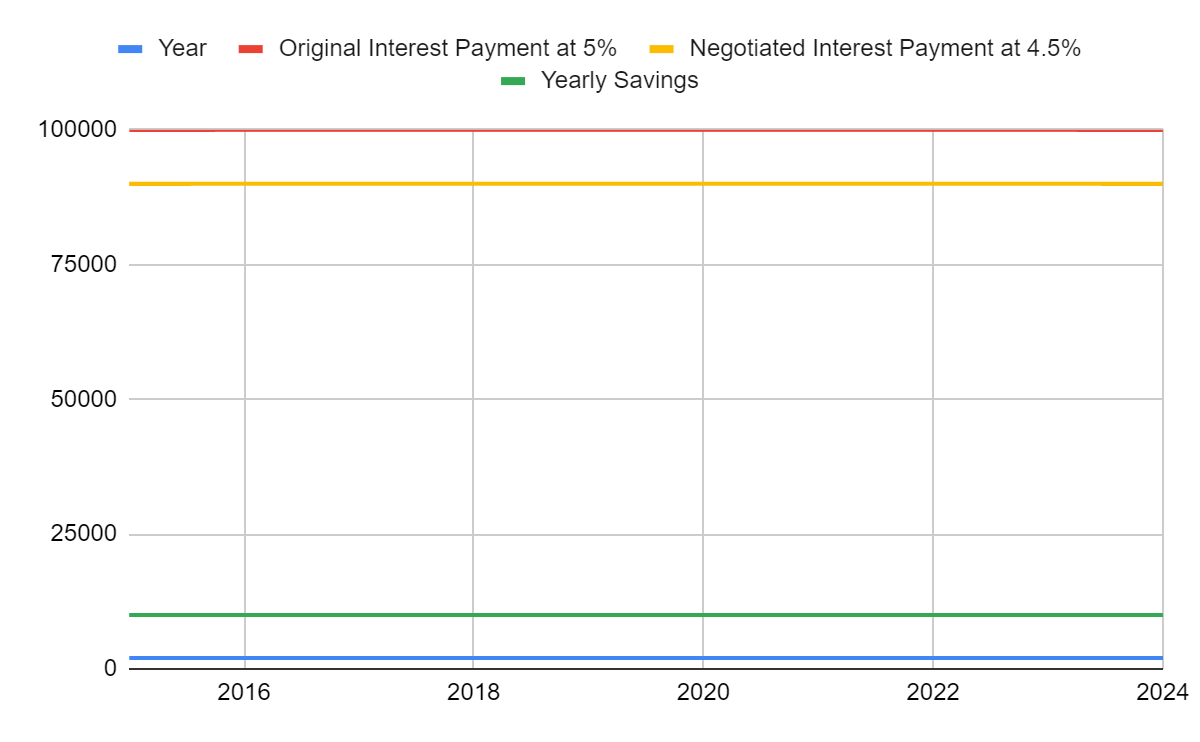

Imagine, for instance, a well-established corporation, say, General Electric, decides to procure a loan for a new manufacturing plant. For simplicity’s sake, let’s ballpark the figure at $50 million. The loan’s interest rate stands at 5%, but then, like an astute player, GE negotiates the rate down to 4.5%.

Kick start your prep by understanding your current financial standing and credit score. Remember, a credit score is akin to your financial reputation. The higher it is, the more eager banks will be to lend to you, and at more favorable rates!

The Negotiation Battle

Think of negotiation as a chess match. You’re the Grandmaster, ready to go into battle armed with your carefully planned strategies. Your first move? Display your improved credit score as a Queen on the board. If it’s risen since you first secured your mortgage, this is your powerful piece that can sway the game in your favor.

On to your next move. Show your adversary – in this case, your lender – the other enticing offers you’ve been scouting. The intel you gathered earlier comes into play now. If Lender A knows that Lender B has a more appealing rate, they might match it to keep you in the game. It’s a smart strategy – just like threatening your opponent’s King with a well-placed Bishop!

Let’s dive into an example. Suppose you’re the CEO of a start-up, ‘Innovation Inc.’ It’s 2023 and you’ve boosted your credit score substantially since your initial loan in 2018. You’re eyeing a new loan offer from ‘Money Tree Capital’ that’s offering a better interest rate. Could you use this as a bargaining chip with your current lender, ‘Dough Flow Banks?’ Absolutely! It’s a powerful move, like shifting your chess piece to put the opposing King in check. The aim is to make Dough Flow Banks match or better the rate offered by Money Tree Capital.

Keep these strategies in mind, dear reader. A well-negotiated loan can be the difference between an ordinary company and a financial powerhouse. Now, go forth and conquer that negotiation table, Grandmaster!

Life After Negotiation

Negotiations done, lower rate in the bag. Time to kick back and bask in your victory, right? Not so fast! You need to keep a vigilant watch on your mortgage, akin to shepherding a flock in a wolf-prone area.

Why? Interest rates are as unpredictable as comic book plot twists. So, stay alert and be prepared to flex your negotiation muscles again if market conditions tilt in your favor. Another hefty saving might just be around the corner!

But if you’re still curious and want a deep dive into the world of mortgages, you might want to check out this comprehensive guide that will walk you through all the details.

FAQS

Can I reduce my mortgage payments?

Absolutely! There are several methods to potentially reduce your mortgage payments:

1. Refinancing: This involves taking out a new loan to pay off your existing mortgage. If the current interest rates are lower than when you took out your original loan, refinancing could reduce your monthly payments.

2. Extending Your Loan Term: Spreading your mortgage payments over a longer term could lower your monthly payments. Keep in mind, though, this may increase the total amount of interest you pay over the life of the loan.

3. Making a Larger Down Payment: If you’re still in the buying process, making a larger down payment could lower your monthly payments by reducing the principal amount of your loan.

4. Removing Private Mortgage Insurance (PMI): If you’ve built up enough equity in your home (usually 20% of the home’s value), you may be able to eliminate your PMI, reducing your monthly payments.

5. Negotiating a Lower Interest Rate: If you have a strong credit score or other qualifying factors, you might be able to negotiate a lower interest rate with your lender, which would reduce your monthly payments.

Remember, each method has its own benefits and potential drawbacks. It’s always a smart move to consult with a financial advisor or mortgage professional to understand what options might be best for your specific situation.

Can a lender change the interest rate after locking?

In most cases, no, a lender cannot change the interest rate after it has been locked. Here’s why:

1. Rate Lock Basics: A rate lock is a guarantee from your lender that they will provide a specific interest rate for your loan, regardless of any fluctuations in the market rate, for a certain period of time until closing.

2. Conditions: However, the rate lock is contingent on certain conditions. If these conditions change, like your credit score drops significantly or the property appraisal is lower than expected, then your rate could potentially change.

3. Lock Expiry: Also, rate locks are time-bound. If your loan doesn’t close before the lock period expires, the lender might adjust your rate to align with the current market rates.

4. Re-Locking: Some lenders allow you to “re-lock” your rate if the market rate drops after you’ve locked in. The policies on this can vary widely from lender to lender.

Remember, it’s essential to get the details of your rate lock in writing and ensure you understand the terms and conditions. If you’re uncertain about anything, don’t hesitate to ask your lender for clarification. They’re there to help guide you through the process.

How to negotiate with a mortgage lender?

Negotiating with a mortgage lender may seem daunting, but with the right approach, you can work towards a deal that suits your financial needs. Here are a few steps to get you started:

1. Know Your Credit Score: Your credit score plays a significant role in the interest rate you’re offered. The higher your score, the better your chances of securing a lower interest rate. If your score has improved, use it as a negotiation tool.

2. Shop Around: Don’t settle for the first offer you receive. Take the time to compare rates and terms from various lenders. Use these offers to bargain for a better deal.

3. Be Prepared: Gather relevant information like your current income, expenses, and the market value of the property. You may also want to prepare a list of questions to ask the lender about the loan terms and fees.

4. Negotiate Points and Fees: Apart from the interest rate, also focus on the points and fees associated with the loan. These can add up and significantly increase your borrowing costs.

5. Ask for Clarifications: If you’re unsure about any part of the offer, don’t hesitate to ask questions. It’s important that you fully understand the terms before signing any agreements.

6. Work with a Broker: If negotiations aren’t your strong suit, consider working with a mortgage broker. They can negotiate on your behalf and possibly secure a better deal than you could alone.

Remember, negotiation is a two-way street. Be honest about your needs and limitations, and you might find your lender more willing to accommodate you.

Can you negotiate mortgages rates on cars?

Mortgages are specifically for real estate properties, like homes. For purchasing cars, we generally deal with auto loans, not mortgages.

However, just like a mortgage, you can indeed negotiate the interest rates on car loans. Here’s a basic guide on how to go about it:

1. Understand Your Credit Score: Your credit score will heavily influence the interest rate you’re offered. A higher score usually leads to lower rates.

2. Shop Around: Before settling on a loan, look at offers from multiple lenders. This includes banks, credit unions, and auto financing companies. Use these offers as a base for negotiation.

3. Pre-Approval Can Help: Getting pre-approved for a loan gives you a better understanding of what rate and terms you can expect. It also strengthens your negotiation position.

4. Negotiate the Price First: Always negotiate the price of the car before discussing the loan terms. Once the price is set, you can then focus on negotiating the interest rate and other loan terms.

5. Read the Fine Print: Ensure you understand all the terms and conditions of your loan, including any fees, penalties, or charges that may apply.

So, while mortgages don’t apply to cars, the principles of negotiation remain the same. Doing your homework and being prepared can help you secure a better deal on your car loan.